Semiconductor Foundry Market Set to Surge to $175.14 Billion by 2025: Key Insights from the U.S., China, and South Korea

Discover how the semiconductor foundry market is projected to reach $175.14B by 2025, driven by innovations and competition between the U.S., China, and South Korea.

- Last Updated:

Semiconductor Foundry Market Forecast for Q1 and Q2 2025

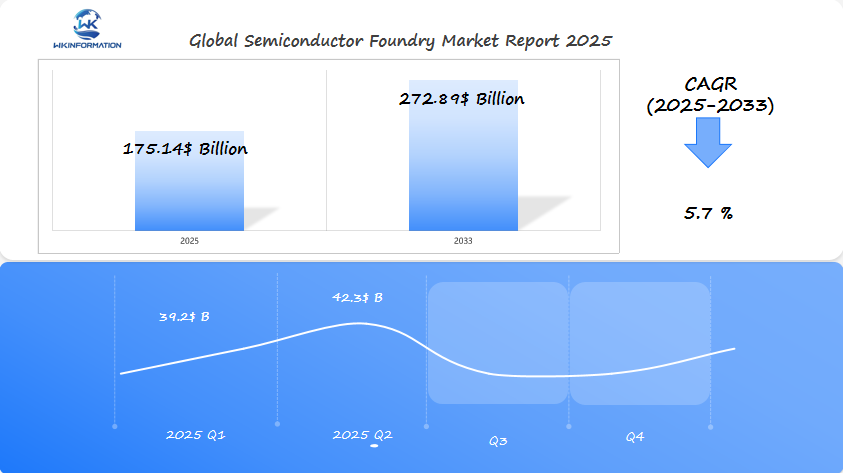

The semiconductor foundry market is projected to reach $175.14 billion in 2025, with a CAGR of 5.7% through 2033. The first half of 2025 is expected to see a steady increase in demand, with Q1 estimated at approximately $39.2 billion and Q2 projected to rise to about $42.3 billion, driven by the growing need for advanced semiconductor manufacturing in industries such as electronics, automotive, and telecommunications.

The U.S., U.K., and Germany are major players in this market. The U.S. leads in both innovation and production, particularly in the tech and automotive industries. The U.K. is investing heavily in semiconductor research and manufacturing as part of its broader digital economy strategy. Germany remains a critical market for semiconductor foundries, fueled by its strong industrial base and automotive sector. These countries are essential for analyzing the global semiconductor foundry landscape.

Exploring the Key Upstream and Downstream Factors Affecting Semiconductor Foundries

The semiconductor foundry ecosystem operates through a complex network of upstream and downstream components that shape the industry’s success and efficiency.

Understanding Upstream vs. Downstream

Upstream activities in semiconductor foundries encompass the essential raw materials, equipment, and processes required for chip manufacturing. Downstream activities involve the distribution channels, customer relationships, and end-user applications that drive market demand.

Critical Upstream Factors

- Raw Materials: The essential materials needed for chip manufacturing, including silicon wafers, specialty gases, photoresist chemicals, high-purity metals, dopants, and other substances.

- Manufacturing Equipment: The tools and machinery used in the production process, such as lithography systems, etching tools, deposition equipment, testing and measurement devices, and clean room infrastructure.

The quality and availability of these upstream components directly impact production yields, chip performance, and manufacturing costs. Supply chain disruptions in upstream factors can create significant bottlenecks in the production process.

Key Downstream Factors

- Customer Demand Drivers: The industries and sectors that drive demand for semiconductors, including consumer electronics manufacturers, automotive companies, telecommunications providers, data center operators, and industrial equipment makers.

- End-User Industry Requirements: The specific needs and specifications of industries that use semiconductors, such as performance requirements, power efficiency needs, form factor constraints, cost targets, and production volume requirements.

Downstream factors shape foundry investment decisions and technology development priorities. Changes in end-user preferences or industry standards can trigger shifts in manufacturing focus and capacity planning.

Supply Chain Integration

Successful semiconductor foundries maintain strong relationships across both upstream and downstream segments. This integration enables:

- Reliable access to critical materials and equipment

- Quick response to changing market demands

- Efficient inventory management

- Reduced production costs

- Enhanced quality control

Understanding these interconnected factors helps foundries optimize their operations and maintain competitive advantages in the rapidly evolving semiconductor market.

Trends Shaping the Growth of the Semiconductor Foundry Market

The semiconductor foundry market’s rapid expansion is driven by three transformative technologies reshaping the industry landscape: AI, IoT, and 5G networks.

Artificial Intelligence and Machine Learning

- AI applications demand highly sophisticated chips with enhanced processing capabilities

- Neural network architectures require specialized semiconductor designs

- Machine learning workloads push the boundaries of traditional chip manufacturing

- Advanced process nodes (7nm, 5nm, 3nm) are essential for AI-optimized semiconductors

Internet of Things Revolution

- Connected devices create unprecedented demand for specialized chips

- IoT semiconductors must balance performance with power efficiency

- Edge computing requirements drive innovation in chip design

- Sensor integration capabilities become crucial for IoT applications

- Custom SoCs (System on Chip) emerge as preferred solutions for IoT devices

5G Network Infrastructure

- High-frequency operations demand cutting-edge semiconductor technology

- RF (Radio Frequency) components require specialized manufacturing processes

- Power amplification modules need advanced thermal management solutions

- Base station equipment relies on complex semiconductor architectures

- Mobile device processors adapt to handle increased data throughput

The intersection of these technologies creates unique manufacturing challenges:

- Enhanced thermal management requirements

- Increased transistor density demands

- Mixed-signal integration complexities

- Power efficiency optimization needs

- Reliability and durability standards

Foundries respond to these trends through:

- Investment in advanced lithography equipment

- Development of specialized process nodes

- Implementation of new materials and techniques

- Creation of dedicated production lines

- Enhanced quality control measures

These technological shifts push foundries to innovate continuously, driving substantial investments in research and development. The demand for specialized chips grows exponentially as AI applications become more sophisticated, IoT devices proliferate, and 5G networks expand their coverage.

Overcoming the Key Barriers to Success in the Semiconductor Foundry Industry

The semiconductor foundry industry faces significant challenges that shape its competitive landscape and market dynamics. These barriers create a complex environment where success requires strategic planning and substantial resources.

1. Capital-Intensive Operations

Setting up a new semiconductor fabrication facility costs between $10-20 billion Advanced equipment like extreme ultraviolet (EUV) lithography machines can exceed $150 million per unit Regular facility upgrades require continuous investment cycles every 2-3 years Maintenance costs for clean rooms and specialized equipment add substantial operational expenses

2. Technological Hurdles

Process node transitions demand extensive R&D investments Current 5nm and 3nm technologies require precise control of atomic-scale features Yield management becomes increasingly complex with smaller semiconductor geometries Heat dissipation and power consumption challenges intensify with denser chip designs

3. Regulatory Landscape

Export controls restrict access to critical manufacturing technologies Environmental regulations mandate specific waste management protocols Safety standards require rigorous compliance measures Intellectual property protection demands sophisticated security systems

The semiconductor foundry market’s entry barriers extend beyond financial considerations. Players must navigate a web of technical complexities while adhering to strict regulatory frameworks. Companies like TSMC and Samsung maintain their market positions through consistent investment in cutting-edge technologies and robust compliance systems.

New market entrants face additional challenges:

- Building relationships with suppliers and customers

- Developing intellectual property portfolios

- Attracting skilled engineering talent

- Establishing quality control systems

Success in the semiconductor foundry industry requires a long-term commitment to technological excellence and operational efficiency. Companies must balance innovation with regulatory compliance while maintaining the financial resources to support ongoing facility modernization.

Geopolitical Dynamics Influencing Semiconductor Foundry Production

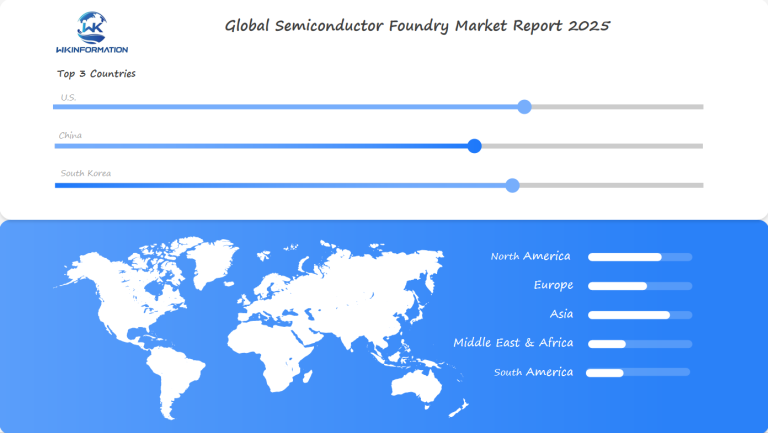

The world of semiconductor foundries has become a complex game of global politics, where countries’ interests collide with the race for technological dominance. The industry’s future is largely influenced by three key players: the United States, China, and South Korea, who are shaping its course through strategic policies and investments.

U.S. Strategic Position

The U.S. is taking significant steps to secure its position in the semiconductor industry:

- Implementing the CHIPS Act with $52 billion in subsidies

- Imposing export restrictions on advanced semiconductor technology to China

- Forming strategic partnerships with allies like South Korea and Japan

- Establishing the “Chip 4 Alliance” to ensure supply chain security

China’s Response

In response to U.S. actions, China is making substantial investments to bolster its domestic semiconductor capabilities:

- Investing $150 billion in developing its own semiconductor industry

- Promoting the “Made in China 2025” initiative to enhance self-sufficiency

- Focusing on creating indigenous intellectual property rights

- Acquiring international semiconductor companies strategically

South Korea’s Balancing Act

South Korea finds itself in a delicate position, trying to balance its relationships with both the U.S. and China:

- Announcing a $450 billion investment plan for its semiconductor sector

- Positioning itself as a neutral player between the two superpowers

- Strengthening its domestic production capabilities

- Cultivating expertise in specialized chip manufacturing

Disruptions Caused by Geopolitical Tensions

The ongoing geopolitical tensions have disrupted traditional supply chains in the semiconductor industry, resulting in several significant changes:

- Reshoring of manufacturing facilities back to home countries

- Establishment of regional semiconductor ecosystems

- Increased emphasis on supply chain resilience and robustness

- Growth of strategic partnerships between nations involved

Trade Policies as Tools in Technological Rivalry

Trade policies have emerged as powerful instruments in this technological competition between nations. The U.S., in particular, has implemented stringent controls on semiconductor exports to China, specifically targeting advanced nodes below 14nm. These restrictions have compelled Chinese manufacturers to expedite their efforts towards developing domestic capabilities by investing heavily in research and development initiatives.

China’s Pursuit of Self-Sufficiency

China’s drive for self-sufficiency in semiconductors involves various key strategies:

- Constructing new fabrication facilities within its borders

- Developing alternative technology standards that do not rely on foreign systems

- Training a specialized workforce skilled in chip design and manufacturing processes

- Establishing domestic supply chains that can support local production needs

Impact on the Global Semiconductor Industry

This geopolitical landscape has far-reaching implications for the global semiconductor industry as a whole:

- Influencing investment decisions made by companies operating across borders

- Shaping technology development priorities based on national interests

- Affecting market access strategies employed by firms seeking entry into specific regions

In this increasingly fragmented market, it becomes imperative for companies to navigate these intricate dynamics while simultaneously maintaining their competitive advantages over rivals.

Deep Dive into Semiconductor Foundry Market Segmentation by Type

The semiconductor foundry market can be divided into two main categories: logic foundries and memory foundries. Each category serves different technological needs and market segments.

Logic Foundries

Logic foundries specialize in manufacturing integrated circuits that perform computational tasks. These facilities produce:

- Microprocessors for computing devices

- Application-specific integrated circuits (ASICs) for specialized functions

- Field-programmable gate arrays (FPGAs) for customizable computing

- System-on-chip (SoC) solutions for mobile devices

Logic foundries hold approximately 65% of the total foundry market share, with TSMC leading the segment at 53% market dominance.

Memory Foundries

Memory foundries focus on producing storage components, including:

- DRAM (Dynamic Random Access Memory) for temporary data storage

- NAND Flash for permanent data storage

- NOR Flash for code storage

- Emerging memory technologies like MRAM and ReRAM

Memory foundries represent about 35% of the market share, with Samsung Electronics and SK Hynix as key players.

Market Distribution by Process Node

The foundry market can also be segmented based on process node technology:

- Advanced nodes (7nm and below): 35% market share

- Intermediate nodes (28nm-10nm): 40% market share

- Mature nodes (40nm and above): 25% market share

Recent industry data shows a shift toward advanced nodes, especially in logic foundries, driven by demands for higher performance and energy efficiency. Memory foundries maintain a balanced approach across different process nodes, adapting to specific storage requirements.

The foundry landscape is constantly evolving with specialized facilities emerging to serve niche markets:

- Analog/mixed-signal foundries

- Power semiconductor foundries

- RF (Radio Frequency) foundries

These specialized segments are growing at different rates, influenced by applications in automotive, IoT, and 5G technologies.

The Role of Applications in Driving Demand for Semiconductor Foundries

The semiconductor foundry market experiences significant demand shifts driven by diverse application sectors. Each sector brings unique requirements and challenges to chip manufacturing processes.

1. Automotive Industry Transformation

- Advanced Driver Assistance Systems (ADAS) require specialized chips capable of real-time processing

- Electric Vehicle (EV) production demands power management semiconductors

- Connected car features need robust communication chips

- Automotive-grade chips must meet strict reliability and durability standards

2. Consumer Electronics Evolution

- Smartphones integrate multiple functions requiring System-on-Chip (SoC) solutions

- Wearable devices push for smaller, energy-efficient chips

- Gaming consoles demand high-performance graphics processors

- Smart home devices need specialized IoT chips

3. Industrial Applications

- Factory automation systems require real-time processing capabilities

- Industrial IoT devices need durable, long-lasting chips

- Smart grid infrastructure demands power management solutions

- Robotics systems integrate multiple chip types for various functions

4. Healthcare Technology

- Medical imaging equipment requires specialized processing units

- Wearable health monitors need energy-efficient chips

- Remote patient monitoring systems demand reliable communication processors

- Medical devices integrate miniaturized semiconductor solutions

5. Data Center Infrastructure

- Cloud computing drives demand for high-performance processors

- Data storage systems need specialized memory chips

- Network equipment requires advanced communication processors

- AI acceleration demands custom chip designs

The application landscape continues to evolve, pushing foundries to develop new manufacturing processes and capabilities. These market demands shape investment decisions in advanced manufacturing technologies and influence capacity planning across the semiconductor industry.

Regional Dynamics: Semiconductor Foundries Across Key Global Markets

The global semiconductor foundry landscape reveals distinct regional patterns and competitive advantages that shape market dynamics. Asia-Pacific commands 65% of the global foundry market share, with Taiwan Semiconductor Manufacturing Company (TSMC) leading the pack.

Asia-Pacific Market Strengths:

- Advanced manufacturing capabilities at 5nm and below

- Established supply chain networks

- Cost-effective labor markets

- Strong government support and incentives

- High concentration of skilled workforce

The region’s dominance stems from decades of strategic investments and infrastructure development. TSMC’s technological prowess enables it to serve high-profile clients like Apple, AMD, and Qualcomm, while Samsung’s facilities in South Korea complement the region’s manufacturing capabilities.

North American Market Position:

- Strong research and development capabilities

- Innovation-driven ecosystem

- Advanced chip design expertise

- Growing government support through initiatives like the CHIPS Act

- Strategic focus on specialized manufacturing

Intel’s presence in North America highlights the region’s emphasis on cutting-edge technology development. The company’s IDM 2.0 strategy aims to revitalize U.S. semiconductor manufacturing through expanded foundry services and modernized facilities.

Regional Competitive Analysis:

Asia-Pacific:

- Manufacturing cost advantage: 15-20% lower than other regions

- Technical workforce density: 3x higher than global average

- Production capacity: 75% of global advanced node manufacturing

North America:

- R&D investment: $25 billion annually

- Patent generation: 35% of global semiconductor patents

- Design expertise: 60% of global chip design revenue

The regional dynamics reflect a complementary relationship between Asia’s manufacturing prowess and North America’s innovation capabilities. Europe maintains a strategic position in specialized semiconductor applications, while emerging markets in Southeast Asia develop their manufacturing capabilities through targeted investments and technology transfers.

U.S. Market: What's Fueling Growth in Semiconductor Foundries?

The U.S. semiconductor industry is experiencing a significant resurgence, propelled by strategic government initiatives and private sector investments. The CHIPS and Science Act has emerged as a game-changing catalyst, allocating $52.7 billion to boost domestic semiconductor manufacturing and research capabilities.

Key growth drivers in the U.S. market include:

1. Federal Support Programs

- $39 billion in manufacturing incentives

- 25% investment tax credit for chip production

- Research and development funding worth $13.2 billion

2. Private Sector Response

- Intel’s $20 billion investment in Arizona facilities

- Samsung’s $17 billion Texas fab expansion

- Micron’s commitment to invest $40 billion through 2030

The U.S. market showcases robust investment trends in advanced chip designs, particularly focusing on:

1. AI/ML Optimization

- Custom-designed chips for machine learning algorithms

- Neural processing units for edge computing

- High-performance computing solutions

2. Edge Computing Infrastructure

- Low-latency processing capabilities

- Energy-efficient chip architectures

- IoT-specific semiconductor designs

These investments align with the national security imperative to secure critical supply chains and maintain technological leadership in emerging fields. The U.S. semiconductor industry’s renewed focus on domestic manufacturing capacity positions it strategically for future growth in advanced computing applications.

China's Dominance in Semiconductor Foundries: What's Next?

China’s semiconductor strategy has evolved into an aggressive push for technological independence. The country’s “Made in China 2025” initiative allocates $150 billion to transform China into a semiconductor manufacturing powerhouse.

Key Strategic Moves:

- Development of domestic foundries like SMIC

- Heavy investment in research and development

- Acquisition of international semiconductor technologies

- Training programs for skilled workforce development

The Chinese government’s self-sufficiency initiatives target 70% domestic chip production by 2025. This ambitious goal drives substantial investments in:

- Advanced manufacturing facilities

- Indigenous intellectual property development

- Local supply chain optimization

- Technical expertise cultivation

Recent developments showcase China’s progress:

SMIC has achieved 7nm chip production capabilities, marking a significant technological breakthrough despite international restrictions.

The nation’s semiconductor landscape faces notable challenges:

- Trade Restrictions: U.S. export controls limit access to advanced manufacturing equipment

- Technical Gaps: Current capabilities lag behind industry leaders TSMC and Samsung

- Talent Pool: Need for experienced semiconductor engineers and designers

China’s market position continues to strengthen through:

- Strategic partnerships with global suppliers

- Focus on specialized chip segments

- Development of alternative manufacturing processes

- Investment in emerging technologies like AI chips

The country’s semiconductor foundry market share is expected to grow from 7.6% to 15% by 2025, driven by domestic demand and increased manufacturing capabilities.

South Korea's Role in the Global Semiconductor Foundry Industry

South Korea is a major player in the global semiconductor industry, thanks to its leading companies, Samsung Electronics and SK Hynix. These two giants have established South Korea as a leader in memory chip production, controlling around 70% of the global DRAM market.

Samsung’s Advances in Foundry Services

Samsung’s semiconductor division has made significant progress in advanced foundry services, offering state-of-the-art process nodes down to 3nm. The company’s strategic investments in research and development have positioned it as a direct competitor to TSMC in the pure-play foundry segment.

Key Strengths of South Korean Foundries

South Korean foundries have several key strengths that contribute to their success:

- Advanced manufacturing capabilities in memory and logic chips

- Strong government support through tax incentives and infrastructure development

- Robust intellectual property protection framework

- Extensive experience in high-volume manufacturing

Government Initiatives to Boost the Semiconductor Industry

The South Korean government’s K-Semiconductor Strategy has pledged $451 billion in investments through 2030, aiming to strengthen the country’s semiconductor ecosystem. This initiative focuses on:

- Expanding production capacity

- Developing next-generation chip technologies

- Building a skilled workforce

- Creating semiconductor clusters

Samsung’s Investment Plans

Samsung’s recent announcement of a $230 billion investment in chip manufacturing facilities near Seoul demonstrates South Korea’s commitment to maintaining its competitive edge. The company plans to establish five new fabs by 2042, focusing on advanced logic chip production and emerging technologies like AI processors.

Collaborations for Innovation

The country’s semiconductor industry benefits from strong partnerships with global technology companies and research institutions, fostering innovation in areas such as:

- Advanced packaging technologies

- 3D NAND development

- High-bandwidth memory solutions

- System-on-chip designs

What Lies Ahead for Semiconductor Foundries?

The semiconductor foundry landscape is set to undergo significant changes by 2030. Industry forecasts suggest that the market value could exceed $300 billion during this period, driven by several key developments:

1. Emerging Technologies

- Quantum computing integration in mainstream chip production

- Advanced packaging solutions for 3D chip stacking

- Silicon photonics for enhanced data processing speeds

- Bio-integrated semiconductors for healthcare applications

2. Manufacturing Innovations

- 2nm and sub-2nm process nodes becoming commercially viable

- AI-powered automated quality control systems

- Smart factory implementations using IoT sensors

- Sustainable manufacturing practices with reduced carbon footprint

The rise of specialized applications creates new market opportunities:

- Automotive-grade chips for autonomous vehicles

- Custom neural processors for edge AI devices

- High-performance computing chips for metaverse infrastructure

- Energy-efficient processors for next-gen mobile devices

Research indicates significant investments in:

- Advanced materials research, including compound semiconductors

- Equipment upgrades for extreme ultraviolet (EUV) lithography

- Talent development programs focused on specialized engineering skills

- Supply chain resilience through geographical diversification

These advancements signal a shift toward more specialized and sophisticated foundry services, with increased focus on customization and application-specific solutions. The industry’s evolution continues to be shaped by technological breakthroughs and changing market demands.

Competitive Landscape: Leading Players in the Semiconductor Foundry Market

The semiconductor foundry market has several dominant players who influence the industry’s direction through technological innovation and manufacturing excellence.

- Taiwan Semiconductor Manufacturing Company (TSMC) – Taiwan

- Samsung Electronics Co. Ltd. – South Korea

- United Microelectronics Corporation (UMC) – Taiwan

- GlobalFoundries (GF) – United States

- Semiconductor Manufacturing International Corporation (SMIC) – China

- Hua Hong Semiconductor – China

- Tower Semiconductor – Israel

- Vanguard International Semiconductor Corporation (VIS) – Taiwan

- Powerchip Semiconductor Manufacturing Corporation (PSMC) – Taiwan

- Nexchip – China

Overall

| Report Metric | Details |

|---|---|

| Report Name | Global Semiconductor Foundry Market Report |

| Base Year | 2024 |

| Segment by Type |

· Logic Foundries · Memory Foundries |

| Segment by Application |

· Automotive · Consumer Electronics · Industrial Applications · Healthcare Technology · Data Center Infrastructure |

| Geographies Covered |

· North America (United States, Canada) · Europe (Germany, France, UK, Italy, Russia) · Asia-Pacific (China, Japan, South Korea, Taiwan) · Southeast Asia (India) · Latin America (Mexico, Brazil) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

The semiconductor foundry industry continues to evolve rapidly, driven by technological advancements, geopolitical factors, and changing market demands. Key success factors include managing upstream supply chains effectively, responding to downstream market needs, and navigating complex international relationships. The industry faces ongoing challenges from capital requirements and technical hurdles, while opportunities emerge from AI, IoT, and 5G applications. Regional dynamics remain crucial, with Asia-Pacific maintaining leadership while other regions invest heavily in domestic capabilities. As the industry moves forward, collaboration between stakeholders, technological innovation, and strategic adaptation to market changes will determine success in this vital sector.

Global Semiconductor Foundry Market Report (Can Read by Free sample) – Table of Contents

Chapter 1: Semiconductor Foundry Market Analysis Overview

- Competitive Forces Analysis (Porter’s Five Forces)

- Strategic Growth Assessment (Ansoff Matrix)

- Industry Value Chain Insights

- Regional Trends and Key Market Drivers

- Vacuum Arc RemeltingMarket Segmentation Overview

Chapter 2: Competitive Landscape

- Global Semiconductor Foundryplayers and Regional Insights

- Key Players and Market Share Analysis

- Sales Trends of Leading Companies

- Year-on-Year Performance Insights

- Competitive Strategies and Market Positioning

- Key Differentiators and Strategic Moves

Chapter 3: Semiconductor Foundry Market Segmentation Analysis

- Key Data and Visual Insights

- Trends, Growth Rates, and Drivers

- Segment Dynamics and Insights

- Detailed Market Analysis by Segment

Chapter 4: Regional Market Performance

- Consumer Trends by Region

- Historical Data and Growth Forecasts

- Regional Growth Factors

- Economic, Demographic, and Technological Impacts

- Challenges and Opportunities in Key Regions

- Regional Trends and Market Shifts

- Key Cities and High-Demand Areas

Chapter 5: Semiconductor Foundry Emerging and Untapped Markets

- Growth Potential in Secondary Regions

- Trends, Challenges, and Opportunities

Chapter 6: Product and Application Segmentation

- Product Types and Innovation Trends

- Application-Based Market Insights

Chapter 7: Semiconductor Foundry Consumer Insights

- Demographics and Buying Behaviors

- Target Audience Profiles

Chapter 8: Key Findings and Recommendations

- Summary ofSemiconductor Foundry Market Insights

- Actionable Recommendations for Stakeholders

Access the study in MULTIPLEFORMATS

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1-866-739-3133

Email: infor@wkinformation.com

What are the key upstream factors affecting semiconductor foundries?

The key upstream factors impacting semiconductor foundries include raw materials and equipment necessary for the production process. These elements are critical as they directly influence the efficiency and quality of chip manufacturing.

How do downstream factors drive the semiconductor market?

Downstream factors such as customer demand and end-user industries significantly drive the need for semiconductor chips. Industries like automotive, consumer electronics, and telecommunications rely heavily on advanced chips, influencing production strategies in foundries.

What role does AI play in the semiconductor foundry market?

AI and machine learning are pivotal in driving demand for advanced semiconductor manufacturing processes. These technologies enable more efficient design and production methods, catering to the growing need for specialized chips in various applications.

What barriers do new entrants face in the semiconductor foundry industry?

New entrants face significant barriers such as high capital expenditures required to establish state-of-the-art fabrication facilities, technological challenges related to evolving process nodes, and regulatory hurdles like export controls and environmental regulations.

How does geopolitical dynamics influence semiconductor foundry production?

Geopolitical dynamics, particularly trade policies and international relations, greatly influence semiconductor foundry production. For instance, U.S. trade policies aim to protect domestic manufacturers while China’s initiatives focus on enhancing self-sufficiency in chip production capabilities.

What are the current trends in regional markets for semiconductor foundries?

The current state of the semiconductor foundry market shows a dominance of the Asia-Pacific region, particularly with major players like TSMC. In contrast, North America is witnessing trends driven by firms like Intel, focusing on technology leadership and skilled workforce availability.

RECENT REPORTS

Our clients