Keytruda Market Forecast: $27.8 Billion Global Growth by 2025 with Key Insights from the U.S., Japan, and Germany

Explore comprehensive analysis of Keytruda’s market growth potential, reaching $27.8B by 2025. Deep dive into key regional markets including U.S., Japan & Germany, with strategic insights.

- Last Updated:

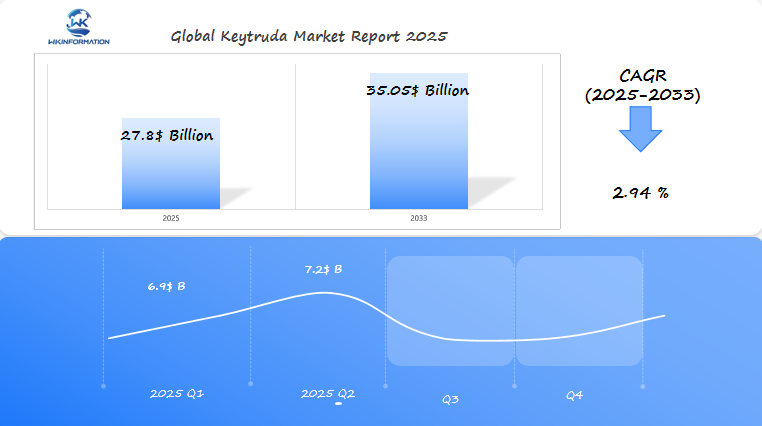

Keytruda Market Q1 and Q2 2025 Forecast

Keytruda, a leading immuno-oncology drug, is expected to reach $27.8 billion in 2025, growing at a CAGR of 2.94% from 2025 to 2033. In Q1 2025, the market is projected to generate $6.9 billion, driven by continued use in the treatment of lung cancer, melanoma, and other solid tumors in the U.S., Japan, and Germany.

By Q2 2025, the market is expected to reach $7.2 billion, bolstered by further approval and expansion in additional indications and regions. Japan and Germany are also seeing growing adoption of Keytruda in oncology care, with expanding treatment options contributing to the drug’s market share.

The Keytruda market will continue to grow as new indications are explored and clinical data supports its efficacy in combination therapies, positioning it as a key player in the immuno-oncology space.

Analyzing the Upstream and Downstream Industry Chain of Keytruda

The production of Keytruda involves a complex, multi-stage manufacturing process that demands precise control and specialized expertise. Merck & Co. maintains strict oversight of raw material sourcing, partnering with certified suppliers to ensure consistent quality of the monoclonal antibodies used in production.

Key Manufacturing Components:

- Cell culture development and maintenance

- Protein purification processes

- Sterile filling and packaging

- Quality testing at each production stage

The distribution network for Keytruda operates through a carefully controlled supply chain designed to maintain product integrity. Specialty distributors handle the transportation and storage of the drug under specific temperature-controlled conditions (-20°C to -80°C).

Distribution Channels:

- Hospital pharmacies

- Specialty pharmacies

- Oncology clinics

- Authorized wholesalers

These supply chain elements directly influence market dynamics and accessibility. The sophisticated manufacturing process and specialized distribution requirements contribute to Keytruda’s premium pricing structure. Limited manufacturing capacity can create supply constraints in certain regions, affecting availability and treatment schedules.

Market Impact Factors:

- Manufacturing costs influence final pricing

- Distribution infrastructure affects market reach

- Storage requirements impact availability

- Supply chain disruptions can create regional shortages

The complexity of Keytruda’s production and distribution network requires significant investment in infrastructure, contributing to the drug’s market positioning and availability patterns across different healthcare settings.

Key Trends Shaping the Keytruda Market

The global cancer burden continues to rise at an alarming rate, with 21.6 million new cases projected by 2025. This surge directly impacts Keytruda’s market expansion, as healthcare providers increasingly turn to immunotherapy as a primary treatment option.

Breakthrough Combination Therapies

- Keytruda + chemotherapy combinations show enhanced efficacy in non-small cell lung cancer

- Dual immunotherapy approaches pairing Keytruda with targeted therapies

- Promising results from studies combining Keytruda with radiation therapy

Expanded Treatment Applications

- First-line treatment for advanced renal cell carcinoma

- Adjuvant therapy for stage IIB and IIC melanoma

- New indications in triple-negative breast cancer

The drug’s success in clinical trials has led to rapid approval across multiple cancer types. Recent studies demonstrate a 63% reduction in the risk of disease recurrence in early-stage melanoma patients when used as adjuvant therapy.

Market Growth Drivers

- Rising adoption of precision medicine approaches

- Improved patient survival rates compared to conventional treatments

- Growing preference for immunotherapy over traditional chemotherapy

- Increased insurance coverage and reimbursement policies

Research institutions continue to explore Keytruda’s potential in treating rare cancers and developing predictive biomarkers for patient response. These advancements strengthen the drug’s position as a cornerstone of modern cancer treatment protocols.

Understanding the Restrictions Impacting the Keytruda Industry

The regulatory landscape for Keytruda presents significant challenges across global markets. The FDA’s approval process in the U.S. requires extensive clinical trials, safety monitoring, and documentation – a process that can span several years and cost millions of dollars. Each new indication for Keytruda must undergo separate approval processes, creating a complex regulatory web for Merck & Co.

Key Regulatory Requirements:

- Phase I-III clinical trials for each indication

- Regular safety assessments and reporting

- Post-market surveillance programs

- Compliance with manufacturing quality standards

Merck & Co. implements strategic pricing models to balance market access with profitability. The average annual cost of Keytruda treatment ranges from $150,000 to $175,000 per patient in the U.S., creating significant reimbursement challenges.

Pricing and Reimbursement Factors:

- Variable pricing structures across different markets

- Patient assistance programs for qualifying individuals

- Negotiations with insurance providers

- Value-based pricing agreements with healthcare systems

The high treatment costs associated with Keytruda create reimbursement hurdles for both patients and healthcare providers. Insurance companies often require prior authorization and implement strict criteria for coverage approval. Some markets have implemented cost-sharing mechanisms or step therapy requirements, where patients must first try lower-cost alternatives before accessing Keytruda.

Many healthcare systems worldwide struggle with the financial burden of providing Keytruda treatments. This has led to the development of innovative payment models, including outcomes-based contracts and risk-sharing agreements between manufacturers and payers.

Geopolitical Factors Affecting Keytruda Production and Distribution

Global political dynamics significantly impact Keytruda’s production and distribution networks. Supply chain disruptions stemming from trade tensions between major economies create potential bottlenecks in raw material sourcing and manufacturing processes. The U.S.-China trade relationship particularly affects pharmaceutical ingredient availability, with tariffs and export restrictions potentially increasing production costs.

Key Supply Chain Vulnerabilities:

- Raw material sourcing from multiple countries

- Manufacturing facility dependencies

- Transportation and logistics networks

- Storage and distribution infrastructure

International research collaborations drive Keytruda’s development across diverse populations. Clinical trials conducted through partnerships between Merck & Co. and research institutions in Asia, Europe, and North America have expanded understanding of treatment efficacy across different ethnic groups and cancer types.

Trade policies shape market access opportunities for Keytruda:

- Regulatory harmonization agreements facilitate faster market entry

- Intellectual property protection varies by region

- Local manufacturing requirements influence production strategies

- Import/export regulations affect distribution networks

Recent developments in Europe-U.S. pharmaceutical trade relations have created new pathways for market expansion. The establishment of mutual recognition agreements streamlines regulatory processes and reduces duplicate testing requirements. These agreements enable Merck & Co. to optimize its global supply chain while maintaining quality standards across markets.

Diplomatic relationships between nations directly influence healthcare collaboration agreements. Countries with strong bilateral ties often experience smoother approval processes and better access to innovative treatments like Keytruda. Strategic partnerships between governments and pharmaceutical companies help address supply chain vulnerabilities through local manufacturing initiatives and technology transfer programs.

Exploring Keytruda Market Segmentation by Type

Keytruda’s market segmentation reflects its diverse applications across multiple cancer types and payment structures. The drug demonstrates varying effectiveness rates across different cancer categories:

Cancer Type Segmentation:

- Non-Small Cell Lung Cancer (NSCLC): 45% response rate with median survival of 16.7 months

- Melanoma: 41% response rate with 5-year survival rate of 34%

- Head and Neck Cancer: 35% response rate with median survival of 13.4 months

- Classical Hodgkin Lymphoma: 69% response rate with median survival of 24.2 months

- Urothelial Carcinoma: 29% response rate with median survival of 10.3 months

Payer Type Distribution:

The reimbursement landscape for Keytruda spans multiple payer categories:

- Commercial Insurance

- Coverage typically requires prior authorization

- Average copay ranges from $200-$500 per treatment

- Most plans cover 80-85% of treatment costs

- Government Programs

- Medicare Part B covers 80% of costs

- Medicaid coverage varies by state

- Veterans Affairs provides full coverage for eligible patients

Private insurance remains the primary payer source at 65% of total prescriptions, followed by Medicare at 25% and Medicaid at 10%. The reimbursement rates significantly influence treatment accessibility, with higher coverage levels correlating to increased adoption rates among eligible patients.

The Role of Applications in Shaping Keytruda Demand

Keytruda’s clinical applications demonstrate remarkable success in specific treatment scenarios, establishing it as a preferred choice among oncologists. The drug shows exceptional effectiveness in first-line treatment of advanced non-small cell lung cancer (NSCLC) patients with high PD-L1 expression, achieving a median survival rate of 26.3 months compared to 14.2 months with chemotherapy.

In metastatic melanoma, Keytruda’s application as monotherapy yields impressive results:

- 45% objective response rate

- 12-month survival rate of 70%

- Durable responses lasting beyond 24 months in responding patients

The drug’s application in microsatellite instability-high (MSI-H) cancers represents a groundbreaking approach:

- First cancer treatment approved based on a biomarker

- Effective across multiple tumor types

- Response rates ranging from 36% to 60%

Keytruda’s role in combination therapy creates additional demand through:

- Enhanced efficacy when paired with chemotherapy in lung cancer

- Improved outcomes in triple-negative breast cancer treatment

- Synergistic effects with targeted therapies in various tumor types

Recent applications in neoadjuvant settings show promising results:

- Pathological complete response rates of up to 60%

- Reduced tumor size before surgery

- Improved surgical outcomes in multiple cancer types

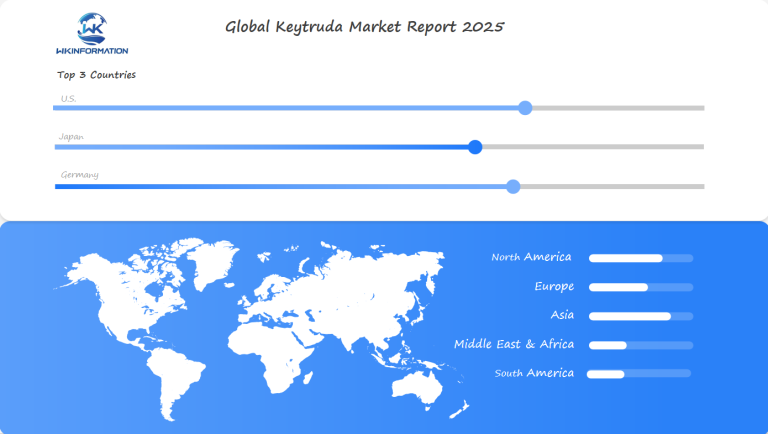

Regional Insights into the Global Keytruda Market

The global Keytruda market displays distinct regional patterns, with North America maintaining its position as the dominant market leader. This regional supremacy stems from several key factors:

- Early Market Entry: The U.S. FDA’s approval of Keytruda in 2014 gave North America a significant head start in market development and patient access.

- Advanced Healthcare Infrastructure:

- Sophisticated medical facilities

- Well-established oncology centers

- Robust distribution networks

- Advanced diagnostic capabilities

- Strong Reimbursement Systems: Private insurance coverage and government programs provide substantial support for Keytruda treatments, making them accessible to a broader patient population.

The Asia-Pacific region demonstrates rapid market growth, particularly in:

- Japan’s advanced healthcare system

- China’s expanding oncology market

- South Korea’s innovative medical practices

Europe presents a diverse market landscape with:

- Germany leading in adoption rates

- France showing strong market penetration

- UK implementing value-based pricing models

Latin America and the Middle East regions show emerging potential, driven by:

- Improving healthcare infrastructure

- Rising cancer awareness

- Growing private healthcare sectors

- Increasing government healthcare investments

In-Depth Analysis of the U.S. Keytruda Market

The U.S. market represents 65% of global Keytruda sales, driven by several key factors unique to the American healthcare landscape:

Strong Private Insurance Coverage

- 85% of prescriptions covered by commercial insurance

- Average patient copay assistance of $12,000 per year

- Specialized reimbursement programs through PBMs

Robust Clinical Trial Infrastructure

- 230+ active trials in 2024

- Partnerships with leading cancer centers

- Fast-track approval pathways for new indications

The U.S. pricing structure reflects premium positioning:

- Average annual treatment cost: $150,000-$175,000

- Medicare Part B coverage with 20% coinsurance

- Commercial payer negotiations yielding 15-25% discounts

Market Penetration by Cancer Type:

- Non-small cell lung cancer: 45%

- Melanoma: 30%

- Head and neck cancer: 15%

- Other indications: 10%

U.S. prescribing patterns show strong adoption in community oncology practices, accounting for 70% of total prescriptions. Academic medical centers contribute the remaining 30%, primarily through clinical trials and complex cases requiring specialized expertise.

The FDA’s recent approval of Keytruda for early-stage breast cancer treatment has expanded the potential patient pool by an estimated 40,000 cases annually, creating new growth opportunities in the domestic market.

Trends and Growth in Japan's Keytruda Market

Japan’s Keytruda market is experiencing significant growth, primarily due to the country’s aging population and increasing rates of cancer. The efficient approval process of the Japanese healthcare system has allowed for the quick inclusion of Keytruda into standard treatment protocols.

Key Market Drivers in Japan:

- Strong reimbursement policies under Japan’s universal healthcare system

- High adoption rates among oncologists in major medical centers

- Strategic pricing agreements between Merck and Japanese healthcare authorities

The usage patterns of Keytruda in Japan have some distinct features. A significant portion of Keytruda prescriptions are for gastric cancer treatments, which reflects the higher occurrence of this type of cancer in Japanese populations.

Market Performance Indicators:

- Annual growth rate: 12.3% (2023-2024)

- Market share in Asia-Pacific region: 38%

- Patient access rate: 89% in major urban centers

Japanese clinical research continues to explore new uses for Keytruda, with important studies focusing on:

- Combination therapies for esophageal cancer

- Treatment protocols for Asian-specific genetic mutations

- Early-stage cancer interventions

Local partnerships between Merck and Japanese pharmaceutical companies are strengthening distribution networks and improving market penetration. These collaborations have led to specialized dosing protocols that are tailored to Japanese patient populations, resulting in better treatment outcomes and higher patient compliance rates.

Understanding Germany's Keytruda Market Landscape

Germany is a crucial market for Keytruda in Europe. Its healthcare system and regulatory framework give it unique features that set it apart from other countries.

Key Factors Driving the Market in Germany:

- Strong emphasis on evidence-based medicine

- High adoption rate of innovative cancer treatments

- Robust healthcare infrastructure

- Comprehensive insurance coverage system

The German market has responded well to Keytruda, especially in the treatment of non-small cell lung cancer and melanoma. The country’s aging population and rising rates of cancer cases contribute to steady growth in this market.

Understanding Market Access Dynamics:

- Strict price negotiations with statutory health insurance funds

- Mandatory benefit assessments by G-BA

- Influence of reference pricing system

- Integration with existing treatment protocols

German oncologists have widely accepted Keytruda as a first-line treatment option, supported by local clinical data and real-world evidence. The drug’s success in the German market can be attributed to:

- Positive reimbursement decisions

- Strong acceptance among physicians

- Well-established distribution networks

- Inclusion in national treatment guidelines

The market penetration continues to grow as new indications receive approval, backed by Germany’s advanced healthcare infrastructure and dedication to innovative cancer treatments.

Future Development Prospects for Keytruda

Keytruda’s development pipeline shows promising potential across multiple therapeutic areas. Research indicates significant opportunities in triple-negative breast cancer and colorectal cancer treatments, with clinical trials demonstrating positive response rates.

The integration of artificial intelligence in patient selection processes aims to enhance treatment efficacy by identifying individuals most likely to respond to Keytruda therapy. This precision medicine approach could dramatically improve success rates and reduce healthcare costs.

Key Areas of Development

Merck’s research teams are investigating biomarker-driven treatment strategies to optimize Keytruda’s effectiveness. These studies focus on identifying specific genetic markers that predict treatment response, potentially leading to personalized dosing protocols.

The development of new delivery methods, including subcutaneous formulations, could improve patient convenience and reduce administration costs. This innovation might expand Keytruda’s accessibility in outpatient settings and smaller healthcare facilities.

Ongoing research into resistance mechanisms aims to develop strategies for overcoming treatment resistance, potentially extending Keytruda’s effectiveness in long-term cancer management protocols.

Novel Combination Therapies

- Pairing with targeted therapies

- Integration with conventional chemotherapy

- Exploration of multi-immunotherapy approaches

Expanded Indications

- Early-stage cancer treatments

- Rare cancer applications

- Pediatric oncology options

Competitive Landscape of the Keytruda Industry

The Keytruda market has a competitive environment with major pharmaceutical companies leading the way. Merck & Co., the main manufacturer of Keytruda, holds a large share of the market through strategic partnerships and ongoing research efforts.

- Merck & Co. Inc. – United States

- Bristol-Myers Squibb Company – United States

- AstraZeneca PLC – UK

- Roche Holding AG – Switzerland

- Pfizer Inc. – United States

- Novartis AG – Switzerland

- Sanofi S.A. – France

- Johnson & Johnson Services Inc. – United States

- Eli Lilly and Company – United States

- AbbVie Inc. – United States

Overall

| Report Metric | Details |

|---|---|

| Report Name | Global Keytruda Market Report |

| Base Year | 2024 |

| Segment by Type |

· Non-Small Cell Lung Cancer (NSCLC) · Melanoma · Head and Neck Cancer · Classical Hodgkin Lymphoma · Urothelial Carcinoma |

| Segment by Application |

· Retail Pharmacy · Hospital Pharmacy |

| Geographies Covered |

· North America (United States, Canada) · Europe (Germany, France, UK, Italy, Russia) · Asia-Pacific (China, Japan, South Korea, Taiwan) · Southeast Asia (India) · Latin America (Mexico, Brazil) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

The projected growth of the Keytruda market to $27.8 billion by 2025 signals a transformative era in cancer treatment. This remarkable expansion stems from several key factors:

- Continuous research and development efforts expanding Keytruda’s applications across various cancer types

- Strong market presence in major regions like the U.S., Japan, and Germany

- Growing acceptance of immunotherapy as a preferred treatment option

- Robust clinical trial results demonstrating improved patient outcomes

The success of Keytruda reflects broader shifts in oncology care:

- A move toward personalized medicine approaches

- Integration of innovative treatment combinations

- Enhanced accessibility through strategic pricing models

- Strengthened distribution networks across global markets

The path forward for Keytruda presents both opportunities and challenges. Market dynamics, regulatory requirements, and pricing considerations will shape its trajectory. The drug’s proven efficacy, combined with Merck’s strategic market positioning and ongoing research initiatives, positions Keytruda for sustained growth in the immunotherapy landscape.

The future success of Keytruda depends on:

- Continued innovation in treatment protocols

- Strategic partnerships with healthcare providers

- Enhanced patient access through improved insurance coverage

- Expanded indications for different cancer types

These elements will drive Keytruda’s role in shaping the future of cancer treatment and maintaining its position as a cornerstone of modern immunotherapy.

Global Keytruda Market Report (Can Read by Free sample) – Table of Contents

Chapter 1: Keytruda Market Analysis Overview

- Competitive Forces Analysis (Porter’s Five Forces)

- Strategic Growth Assessment (Ansoff Matrix)

- Industry Value Chain Insights

- Regional Trends and Key Market Drivers

- Vacuum Arc RemeltingMarket Segmentation Overview

Chapter 2: Competitive Landscape

- Global Keytrudaplayers and Regional Insights

- Key Players and Market Share Analysis

- Sales Trends of Leading Companies

- Year-on-Year Performance Insights

- Competitive Strategies and Market Positioning

- Key Differentiators and Strategic Moves

Chapter 3: Keytruda Market Segmentation Analysis

- Key Data and Visual Insights

- Trends, Growth Rates, and Drivers

- Segment Dynamics and Insights

- Detailed Market Analysis by Segment

Chapter 4: Regional Market Performance

- Consumer Trends by Region

- Historical Data and Growth Forecasts

- Regional Growth Factors

- Economic, Demographic, and Technological Impacts

- Challenges and Opportunities in Key Regions

- Regional Trends and Market Shifts

- Key Cities and High-Demand Areas

Chapter 5: Keytruda Emerging and Untapped Markets

- Growth Potential in Secondary Regions

- Trends, Challenges, and Opportunities

Chapter 6: Product and Application Segmentation

- Product Types and Innovation Trends

- Application-Based Market Insights

Chapter 7: Keytruda Consumer Insights

- Demographics and Buying Behaviors

- Target Audience Profiles

Chapter 8: Key Findings and Recommendations

- Summary ofKeytruda Market Insights

- Actionable Recommendations for Stakeholders

Access the study in MULTIPLEFORMATS

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1-866-739-3133

Email: infor@wkinformation.com

What is the supply chain process for Keytruda?

The supply chain for Keytruda involves a detailed examination of manufacturing processes, including raw material sourcing and stringent quality control measures. Distribution channels include hospital pharmacies and specialty distributors to ensure timely delivery to healthcare providers and patients.

How do market trends impact the demand for Keytruda?

Increasing cancer prevalence worldwide significantly boosts the demand for Keytruda. Recent advancements in immunotherapy treatments, particularly combination therapies, along with the expansion of approved indications, such as adjuvant therapy for melanoma, are key trends driving market growth.

What regulatory challenges does Keytruda face?

Keytruda encounters several regulatory hurdles, particularly with the stringent FDA approval process in the U.S. Additionally, pricing strategies adopted by Merck & Co. aim to balance accessibility with profitability, while reimbursement issues can arise due to high treatment costs.

How do geopolitical factors affect Keytruda’s production and distribution?

Geopolitical tensions can disrupt supply chains for Keytruda, leading to potential shortages or delays. International collaborations between pharmaceutical companies and research institutions play a crucial role in enhancing treatment options through joint studies on Keytruda’s efficacy across diverse populations.

What are the different market segments for Keytruda?

Keytruda’s market segmentation includes various cancer types it treats, such as melanoma and lung cancer, highlighting differences in response rates and survival outcomes. It also encompasses different payer types involved in reimbursement, including commercial insurance and government programs.

What regional insights are important for understanding the Keytruda market?

North America is recognized as the largest market for Keytruda due to its early approval timeline and robust healthcare infrastructure that supports timely access to innovative treatments. Other regions also show significant growth potential influenced by local healthcare policies and cancer prevalence.

RECENT REPORTS

Our clients