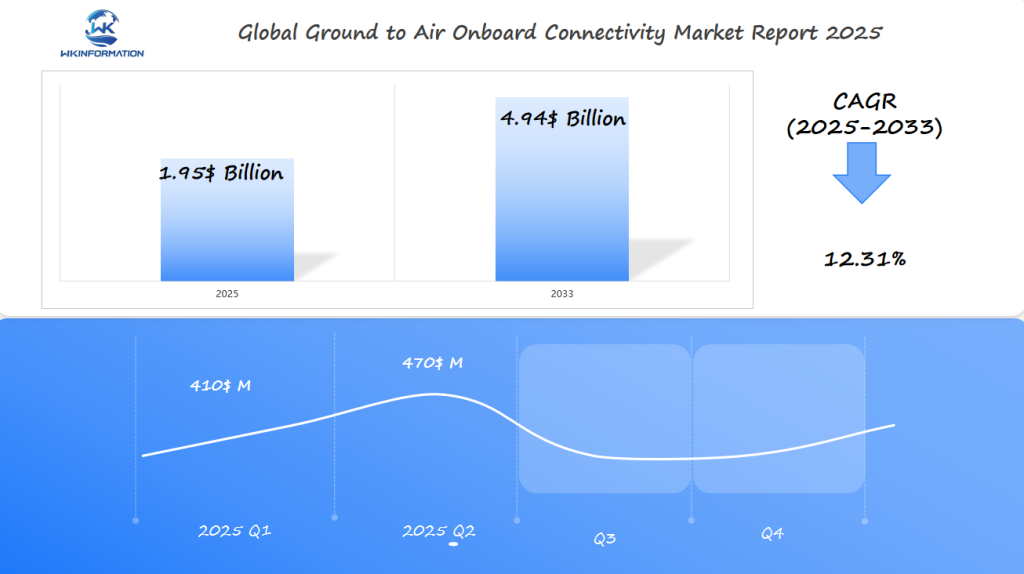

Ground to Air Onboard Connectivity Market Projected to Hit $1.95 Billion Worldwide in 2025: Strong Momentum in the U.K., India, and Japan

Ground to Air Onboard Connectivity Market overview highlighting the ecosystem’s upstream hardware manufacturers, satellite providers, and ground infrastructure operators, alongside downstream stakeholders like airlines and OEMs.

- Last Updated:

Ground to Air Onboard Connectivity Market Q1 and Q2 of 2025 Forecast and Regional Focus

The Ground to Air Onboard Connectivity market is expected to reach $1.95 billion by 2025, driven by a strong CAGR of 12.31% through 2033. Early 2025 sales are projected to be uneven, with Q1 around $410 million, rising to $470 million in Q2, reflecting accelerating adoption in commercial aviation and defense sectors.

The U.K. is a major player due to its leading aerospace industry and regulatory support, while India’s rapidly growing aviation market fuels demand for onboard connectivity solutions. Japan’s focus on technological innovation and passenger experience further bolsters the market. These regions are essential to track for evolving regulatory frameworks, technological advancements, and growing passenger expectations.

Mapping the Upstream and Downstream Ecosystem of Ground to Air Onboard Connectivity

The Ground to Air Onboard Connectivity Market operates through a complex, multi-tier supply chain that ensures seamless inflight communication infrastructure for airlines and passengers. The ground to air connectivity ecosystem involves a variety of stakeholders, each playing a distinct role in enabling high-speed internet and data services onboard aircraft.

Upstream: Building the Foundation

Key upstream components form the backbone of the onboard connectivity supply chain:

- Hardware Manufacturers: These companies design and produce specialized equipment such as antennas, modems, routers, and cabin wireless access points. Notable players include Panasonic Avionics, Collins Aerospace, and Honeywell International.

- Satellite Providers: Firms like Inmarsat, Viasat, and SpaceX deliver satellite bandwidth and network capacity for consistent global coverage. Their networks—GEO (Geostationary), MEO (Medium Earth Orbit), or LEO (Low Earth Orbit)—define the speed and reach of inflight services.

- Ground Infrastructure Operators: Data centers, ground stations, and terrestrial networks support signal relay between satellites or dedicated air-to-ground towers and aircraft in flight. Efficient ground infrastructure is critical for low-latency connections.

Downstream: Delivering Value

Downstream stakeholders transform hardware and connectivity into passenger-facing services:

- Airlines: Responsible for selecting vendors, integrating systems into their fleets, and offering tailored connectivity packages for passengers.

- Aircraft OEMs (Original Equipment Manufacturers): Airbus, Boeing, Embraer, and others integrate onboard connectivity hardware at the production stage or enable later retrofits.

- Maintenance Service Providers: Ensure continuous operation by maintaining, upgrading, or troubleshooting connectivity systems post-installation.

- End Passengers: The ultimate beneficiaries—demanding high-speed Wi-Fi, real-time updates, streaming entertainment, and personalized content during flights.

Technology Integrators & System Installers

Technology integrators bridge upstream innovations with airline operations. These specialists handle system design, certification processes (meeting stringent aviation standards), installation on new builds or existing fleets, testing protocols, and ongoing technical support. Their expertise determines integration speed and reliability—a decisive factor as airlines modernize inflight communication infrastructure.

Emerging Trends and Innovations Shaping the Ground to Air Onboard Connectivity Market

Integration of 5G with air-to-ground communication systems for enhanced bandwidth

The introduction of 5G technology into air-to-ground communication systems is changing the game for onboard connectivity. This integration provides significantly higher bandwidth, allowing passengers to experience faster internet speeds and more reliable connections during flights. This enhancement supports various applications such as streaming high-definition videos, real-time gaming, and seamless video conferencing.

Adoption of multi-orbit satellite networks (GEO/MEO/LEO) expanding coverage and reliability

To improve connectivity coverage and reliability, multi-orbit satellite networks are being adopted. These networks include Geostationary Orbit (GEO), Medium Earth Orbit (MEO), and Low Earth Orbit (LEO) satellites. GEO satellites offer broad coverage, MEO satellites provide lower latency, while LEO satellites ensure rapid data transmission due to their proximity to Earth. With these combined capabilities, uninterrupted internet access can be delivered even in the most remote flight paths.

Development of wireless streaming technologies including VR/AR applications onboard aircraft

Wireless streaming technologies have advanced significantly, enabling new forms of inflight entertainment such as Virtual Reality (VR) and Augmented Reality (AR). These immersive experiences enhance passenger satisfaction by providing captivating content that can be accessed through personal devices or airline-provided headsets. VR/AR applications bring a new dimension to inflight entertainment, making long-haul flights more engaging.

Cloud-based content delivery platforms improving passenger experience and operational efficiency

Cloud-based content delivery platforms are transforming how airlines manage inflight entertainment and connectivity services. These platforms allow for dynamic content updates, personalized passenger experiences, and efficient data management. Passengers benefit from a vast selection of media accessible on-demand, while airlines gain operational efficiency through streamlined content distribution and real-time analytics.

This section highlights key innovations reshaping the ground to air onboard connectivity space:

- The integration of 5G technology boosts bandwidth capabilities

- Multi-orbit satellite networks ensure comprehensive coverage

- Wireless streaming technologies introduce VR/AR applications

- Cloud-based platforms enhance both passenger experience and airline operations

Critical Restrictions Impacting Ground to Air Onboard Connectivity Industry Growth

Financial Barriers

The ground to air onboard connectivity market faces significant financial barriers due to the high implementation costs associated with advanced hardware and installation processes. Aircraft fleets require costly components like satellite antennas, communication modules, and routers to enable seamless connectivity. The initial investment for these technologies is substantial, often leading airlines to hesitate in upgrading their systems.

Regulatory Challenges

Regulatory hurdles are another critical restriction impacting industry growth. Aviation safety compliance and stringent data security protocols must be met to ensure passenger safety and information protection. These regulations vary significantly across countries, creating complex challenges for global connectivity providers aiming to standardize services.

Compatibility Issues

Integrating new systems with older or legacy aircraft models presents notable compatibility issues. Many airlines operate fleets consisting of various aircraft types and ages, making uniform upgrades challenging. Compatibility difficulties arise when trying to match cutting-edge connectivity technologies with existing avionics, which can delay modernization efforts and increase costs.

Limited Ground Infrastructure Coverage

In remote or less developed regions, limited ground infrastructure coverage affects service continuity significantly. The absence of robust ground stations and support systems restricts the availability and reliability of onboard connectivity solutions in these areas. Passengers flying over sparsely populated or rural regions often experience disruptions in internet access due to inadequate infrastructure support.

Addressing these critical restrictions requires strategic investments, regulatory harmonization, innovative solutions for legacy systems integration, and expanded ground infrastructure development in underserved areas. These efforts will be pivotal in overcoming the current barriers and unlocking the full potential of the ground to air onboard connectivity market.

Analyzing Geopolitical Influences on the Ground to Air Onboard Connectivity Sector

Geopolitical factors significantly influence the Ground to Air Onboard Connectivity Market. Here’s how:

1. International Aviation Regulations

International aviation regulations—such as those from ICAO, EASA, and the FAA—set requirements for onboard communications that must be followed across borders. Airlines operating international routes need to adhere to different regulatory frameworks, which directly impacts the implementation of connectivity solutions.

2. Government Modernization Programs

Government initiatives aimed at modernization drive growth in the market. Investments in advanced airspace management systems and digital infrastructure create favorable conditions for the adoption of next-generation inflight connectivity. For instance:

- The U.K.’s Future Flight Challenge supports digital upgrades and connected aviation corridors.

- India’s Digital Sky initiative fosters regulatory support for connected aircraft across its growing domestic sector.

3. Trade Policies

Trade policies can present both opportunities and challenges. Tariffs or export restrictions on semiconductor components, network hardware, and encryption technologies affect how original equipment manufacturers (OEMs) and system integrators source their materials. Changes in policy can disrupt established supply chains or open up new possibilities for innovation through international technology partnerships.

4. Strategic Partnerships

Countries are increasingly forming strategic partnerships to enhance satellite internet capabilities for aviation. Joint ventures—such as those between European operators and Asian satellite providers—expand network coverage, balance costs, and ensure reliable service over long-distance routes.

These geopolitical factors influence technology access, deployment strategies, and ultimately shape the passenger experience in the global onboard connectivity ecosystem.

Understanding the Market: Types and Distribution of Ground to Air Onboard Connectivity

Knowing the market well is crucial for gaining an edge in the ground to air onboard connectivity industry. By breaking things down into specific categories, we can see where the opportunities are.

1. Types of Hardware Used

When it comes to hardware, there are three main types:

- Inflight Entertainment Systems (IFE): These systems offer video, audio, and interactive content, serving as the foundation for digital experiences enjoyed by passengers.

- Communication Modules: These specialized avionics enable real-time data transmission between aircraft and ground stations.

- Routers: High-capacity devices installed onboard that efficiently manage network traffic, ensuring a stable Wi-Fi connection throughout the cabin.

2. Connectivity Technologies

There are two primary models for connectivity technologies:

- Satellite-Based Solutions: These systems utilize GEO, MEO, or LEO satellites to provide coverage. They are particularly effective on long-haul and transoceanic routes where ground infrastructure is limited. Airlines rely on global coverage from satellites to offer uninterrupted service.

- Air-to-Ground (ATG) Connectivity: In this model, ground-based towers communicate directly with aircraft antennas. ATG is ideal for domestic or regional flights that operate over land areas. It offers high bandwidth and low latency but has geographical limitations.

3. Aircraft Categories

Narrow-body planes like the Airbus A320 and Boeing 737 families are the most common aircraft used for short and medium-haul operations. This dominance creates a strong demand for scalable connectivity solutions specifically designed for high-frequency routes.

4. End-User Segmentation

There are two types of end-user segmentation:

- OEM Installations: These systems are factory-fitted and integrated during the production of aircraft. They are preferred by full-service airlines that prioritize long-term reliability.

- Aftermarket Retrofit Upgrades: These upgrades are installed on existing fleets to modernize older aircraft and meet changing passenger expectations.

Understanding these different segments helps guide technology investments and reveals growth opportunities in various areas of aviation.

Exploring Application-Driven Demand in Ground to Air Onboard Connectivity Solutions

The demand for ground to air onboard connectivity solutions is being driven by several key applications that enhance both passenger experience and operational efficiency:

- Increasing passenger expectations for high-speed internet access during flights worldwide: Modern travelers expect seamless internet connectivity at all times, including during flights. This demand has led airlines to invest heavily in onboard Wi-Fi systems capable of providing strong and reliable connections.

- Utilization of ground to air connectivity for real-time flight tracking and operational data analytics: Airlines use these technologies to monitor aircraft performance, track flight paths, and gather critical operational data in real-time. This information helps improve safety, optimize routes, and enhance overall efficiency.

- Enhancement of maintenance efficiency via continuous data transmission from airborne units: Continuous data transmission allows airlines to perform predictive maintenance, monitor system health, and address potential issues before they become critical. This leads to reduced downtime and improved fleet reliability.

- Expanding inflight entertainment offerings enabled by seamless connectivity solutions: Passengers can enjoy a wide range of entertainment options including live TV, movies, music streaming, and interactive applications. Advanced connectivity solutions enable these services to be delivered smoothly without interruption.

These applications underscore the importance of robust ground to air connectivity systems in meeting the evolving demands of both passengers and airlines.

Regional Breakdown of the Global Ground to Air Onboard Connectivity Market Landscape

North America: The Dominant Player

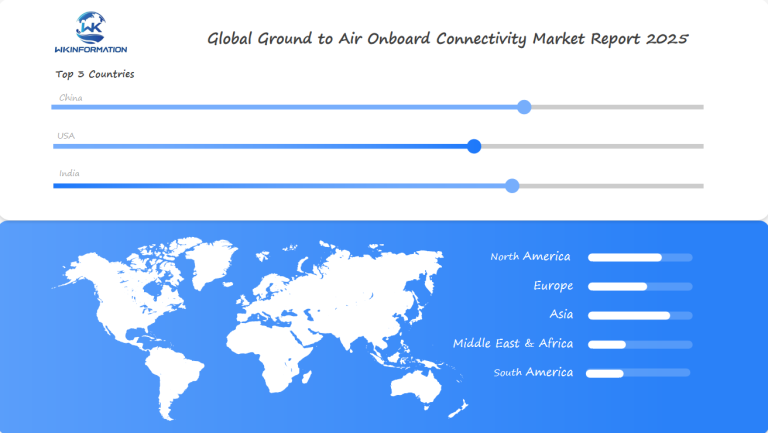

North America, particularly the U.S., holds a dominant position, capturing roughly 75% of the revenue share. This is attributed to its mature market and extensive aviation infrastructure.

Asia-Pacific: The Rapidly Expanding Region

In the Asia-Pacific region, there is rapid expansion driven by a large population base and an increasing middle class. Countries such as India and Japan are leading this growth due to their burgeoning aviation sectors and technological advancements.

Europe: The Evolving Market

Europe showcases growing demand influenced by technological advances and evolving consumer preferences. The region’s focus on enhancing passenger experience through advanced onboard connectivity solutions contributes significantly to market growth.

This regional market analysis highlights varied growth drivers across different geographies, emphasizing the global momentum in onboard connectivity solutions. The strong performance in North America sets a benchmark while Asia-Pacific’s potential showcases future opportunities, and Europe’s advancements illustrate technological progress.

Insights into the U.K. Ground to Air Onboard Connectivity Market Developments

The U.K. inflight connectivity growth story is marked by aggressive investments in both satellite-based internet services and advanced air-to-ground communication systems. National carriers and low-cost airlines are prioritizing passenger satisfaction, driving rapid adoption of high-speed onboard Wi-Fi across both domestic and international fleets. British Airways, Virgin Atlantic, and easyJet have rolled out next-generation Wi-Fi platforms, responding directly to rising consumer expectations for uninterrupted digital access at 35,000 feet.

Key factors shaping the market:

- Satellite investments UK: British infrastructure providers and telecom giants are collaborating with global leaders such as Inmarsat and Eutelsat, enhancing network capacity and service availability over U.K. airspace. The push toward multi-orbit satellite constellations also positions the U.K. as a front-runner in consistent, high-bandwidth inflight connectivity.

- Airline technology adoption UK: Fleet upgrades focus on integrating modular connectivity hardware that supports streaming, real-time messaging, and BYOD entertainment models. These initiatives address both premium cabin and budget traveler needs.

- Government support: National modernization strategies include funding for digital infrastructure upgrades at airports and incentives for airlines investing in cutting-edge connectivity solutions.

- Industry collaboration: Partnerships between local tech firms—such as Cobham—and global aerospace players accelerate the delivery of innovative solutions tailored to the unique regulatory and operational environment of U.K. aviation.

The U.K.’s blend of policy support, technological ambition, and consumer-centric airline strategies places it at the forefront of European inflight connectivity advancements.

India’s Rapidly Expanding Ground to Air Onboard Connectivity Market

The growth of India’s onboard connectivity market is accelerating as rising disposable income transforms travel expectations. A surge in the middle-class traveler base has led to increased demand for seamless inflight Wi-Fi in India, pushing airlines to prioritize investment in state-of-the-art connectivity solutions.

Key Drivers of Growth

Several factors are driving the growth of the onboard connectivity market in India:

- Fleet Upgrades by Domestic Carriers: Airlines like IndiGo and Vistara are actively upgrading their fleets with advanced inflight connectivity equipment such as next-generation antennas and high-throughput modems.

- Government Initiatives for Digital Transformation: The government’s focus on digital transformation in aviation, through initiatives like DigiYatra and updated regulatory frameworks, is facilitating wider adoption of onboard internet services.

- Partnerships with Satellite Service Providers: Strategic agreements with global satellite service providers, including partnerships with Inmarsat and Hughes Communications India, are expanding coverage across the country’s vast airspace. This ensures reliable connections not only for major metro routes but also for underserved regional corridors.

Passenger expectations have shifted noticeably—travelers now consider high-speed inflight Wi-Fi a standard amenity rather than a luxury. Airlines responding to this shift are leveraging connectivity as a key competitive differentiator, using it to boost customer loyalty while enabling new revenue streams through entertainment and e-commerce platforms. The trajectory of the Indian market positions it as a dynamic hub for ongoing innovation in ground to air onboard solutions.

Japan’s Strategic Advances in Ground to Air Onboard Connectivity Technologies

Japan is leading the way in inflight connectivity innovation, with a focus on integrating advanced satellite communications into its airlines’ fleets. This strategic approach aims to provide a top-notch passenger experience through high-speed internet access onboard.

Key developments include:

- Collaboration between tech giants and aviation companies: Major players are driving research and development efforts to improve connectivity solutions. Partnerships between these entities ensure continuous innovation and deployment of advanced technologies.

- Government-supported projects: These initiatives assist in modernizing airspace, making it easier to install and operate complex systems onboard.

- Use of multi-orbit satellite networks: By leveraging GEO, MEO, and LEO satellites, Japanese airlines can provide dependable and widespread coverage, guaranteeing smooth connectivity regardless of flight routes.

- Focus on passenger experience: Airlines are prioritizing fast internet for passengers, enhancing their overall travel experience with uninterrupted streaming and real-time communication capabilities.

These efforts position Japan strongly in the Ground to Air Onboard Connectivity Market, setting a standard for technological progress and passenger satisfaction in aviation.

Future Outlook and Innovation in Ground to Air Onboard Connectivity

The future of the ground to air onboard connectivity market is looking bright, with expected growth and new technologies on the horizon. Industry experts predict that the global inflight connectivity (IFC) market will exceed USD 18 billion by 2034, driven mainly by changing passenger needs. Airlines are now focusing more on providing seamless, high-speed internet access and personalized digital experiences, raising the bar for future inflight systems.

Key Factors Driving Future Market Growth:

- Changing Passenger Expectations: More and more passengers want to stream content without interruptions, communicate in real-time, and work remotely while flying. In response, airlines are investing in systems that can handle these high-demand applications.

- Advanced Inflight Systems: The next generation of IFC solutions combines cutting-edge hardware and software to cater to both passenger entertainment and airline operational requirements.

New Technologies Shaping the IFC Market:

- Multi-Orbit Satellite NetworksCompanies are using a combination of GEO (Geostationary), MEO (Medium Earth Orbit), and LEO (Low Earth Orbit) satellites to create hybrid networks.

- This strategy improves global coverage and reliability, particularly on long-haul flights over oceans where ground infrastructure is limited.

- Projects like SpaceX’s Starlink Aviation and OneWeb’s partnerships in aviation demonstrate this shift.

- AI-Powered Data AnalysisArtificial intelligence is being used in network management systems to enhance connection performance onboard.

- AI algorithms can anticipate periods of high usage, adjust bandwidth allocation on-the-fly, and resolve service interruptions instantly.

- Airlines can use predictive analysis for proactive maintenance, minimizing downtime and boosting overall service quality.

- VR/AR Immersive EntertainmentVirtual reality (VR) and augmented reality (AR) technologies have the potential to revolutionize inflight entertainment.

- Passengers will have access to immersive experiences such as interactive games or virtual tours of destinations, all made possible through speedy onboard networks.

- Initial trials conducted by major airlines indicate a move towards unique cabin experiences tailored for tech-savvy travelers.

Ongoing investment in research and development drives these trends forward, placing the ground to air connectivity industry at the forefront of aviation innovation. The combination of advanced satellite networks, AI-driven analytics, and immersive digital content signifies a new chapter for both airlines and their customers.

Key Competitors and Market Leaders in Ground to Air Onboard Connectivity

The Ground to Air Onboard Connectivity Market is highly competitive, with a few global technology leaders at the forefront. These companies are constantly pushing boundaries through product innovation, strategic partnerships, and significant investments in research and development.

- Thales Group – France

- Gogo Inc. – United States

- Panasonic Avionics Corporation – United States

- Viasat Inc. – United States

- Collins Aerospace – United States

- Honeywell Aerospace – United States

- Inmarsat – United Kingdom

- Global Eagle Entertainment – United States

- SmartSky Networks – United States

- Astronics Corporation – United States

Overall

| Report Metric | Details |

|---|---|

| Report Name | Global Ground to Air Onboard Connectivity Report |

| Base Year | 2024 |

| Segment by Type |

· Inflight Entertainment Systems (IFE) · Communication Modules · Routers |

| Segment by Application |

· Commercial Aviation · Business Aviation · Military & Defense Aviation · Cargo & Freight Aviation |

| Geographies Covered |

· North America (United States, Canada) · Europe (Germany, France, UK, Italy, Russia) · Asia-Pacific (China, Japan, South Korea, Taiwan) · Southeast Asia (India) · Latin America (Mexico, Brazil) |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |

The Ground to Air Onboard Connectivity Market is set for significant growth, driven by advancements in communication technologies and increasing passenger expectations for seamless connectivity. Key industry players like AT&T, Panasonic Avionics Corporation, and Honeywell International Inc. continue to lead through strategic investments and innovative solutions.

Global Ground to Air Onboard Connectivity Market Report (Can Read by Free sample) – Table of Contents

Chapter 1: Ground to Air Onboard Connectivity Market Analysis Overview

- Competitive Forces Analysis (Porter’s Five Forces)

- Strategic Growth Assessment (Ansoff Matrix)

- Industry Value Chain Insights

- Regional Trends and Key Market Drivers

- Women’s ActivewearMarket Segmentation Overview

Chapter 2: Competitive Landscape

- GlobalGround to Air Onboard Connectivity players and Regional Insights

- Key Players and Market Share Analysis

- Sales Trends of Leading Companies

- Year-on-Year Performance Insights

- Competitive Strategies and Market Positioning

- Key Differentiators and Strategic Moves

Chapter 3: Ground to Air Onboard Connectivity Market Segmentation Analysis

- Key Data and Visual Insights

- Trends, Growth Rates, and Drivers

- Segment Dynamics and Insights

- Detailed Market Analysis by Segment

Chapter 4: Regional Market Performance

- Consumer Trends by Region

- Historical Data and Growth Forecasts

- Regional Growth Factors

- Economic, Demographic, and Technological Impacts

- Challenges and Opportunities in Key Regions

- Regional Trends and Market Shifts

- Key Cities and High-Demand Areas

Chapter 5: Ground to Air Onboard Connectivity Emerging and Untapped Markets

- Growth Potential in Secondary Regions

- Trends, Challenges, and Opportunities

Chapter 6: Product and Application Segmentation

- Product Types and Innovation Trends

- Application-Based Market Insights

Chapter 7: Ground to Air Onboard Connectivity Consumer Insights

- Demographics and Buying Behaviors

- Target Audience Profiles

Chapter 8: Key Findings and Recommendations

- Summary ofWomen’s ActivewearMarket Insights

- Actionable Recommendations for Stakeholders

Access the study in MULTIPLEFORMATS

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1-866-739-3133

Email: infor@wkinformation.com

What are the key components of the ground to air onboard connectivity ecosystem?

The ground to air onboard connectivity ecosystem comprises upstream hardware manufacturers, satellite providers, and ground infrastructure operators, along with downstream stakeholders such as airlines, aircraft OEMs, maintenance service providers, and end passengers. Technology integrators and system installers play a crucial role in ensuring seamless connectivity within this supply chain.

How is 5G integration transforming the ground to air onboard connectivity market?

5G integration enhances air-to-ground communication systems by providing higher bandwidth and improved data speeds. This advancement supports emerging technologies like VR/AR inflight entertainment and cloud content management platforms, thereby significantly enriching passenger experience and operational efficiency in the onboard connectivity market.

What are the main challenges restricting growth in the ground to air onboard connectivity industry?

Growth is constrained by high implementation costs due to expensive hardware and installation on aircraft fleets, regulatory hurdles related to aviation safety compliance and data security, compatibility issues with legacy aircraft models, and limited ground infrastructure coverage in remote regions that affect continuous service availability.

How do geopolitical factors influence the ground to air onboard connectivity sector?

Geopolitical influences include international aviation regulations impacting cross-border connectivity solutions, government modernization programs upgrading airspace infrastructure, trade policies affecting global component sourcing and technology collaborations, and strategic partnerships between countries enhancing satellite internet capabilities for aviation.

What are the emerging trends shaping the future of ground to air onboard connectivity?

Emerging trends include adoption of multi-orbit satellite networks (GEO/MEO/LEO) for expanded coverage and reliability, development of wireless streaming technologies including VR/AR applications onboard aircraft, cloud-based content delivery platforms improving passenger experience, and AI-enabled data analytics optimizing network performance for next-generation inflight systems.

Which regions dominate the global ground to air onboard connectivity market and why?

The U.S. dominates with approximately 75% revenue share due to its mature market status. Asia-Pacific is experiencing rapid expansion driven by a large population base and rising middle class. Europe shows growing demand fueled by technological advances and consumer preferences. Additionally, countries like the U.K., India, and Japan are making significant strides through investments in satellite services, airline technology adoption, and government modernization initiatives.

RECENT REPORTS

Our clients